It’s Time for Businesses to Rethink Their Working Capital Practices

In today’s uncertain marketplace, businesses are being forced to re-evaluate their working capital needs. Some managers have learned the hard way during the pandemic that operating “lean” has its limits.

What Is Working Capital?

Working capital — current assets minus current liabilities — is traditionally a measure of liquidity. It’s the amount of

money you need in order to support your short-term business operations. It helps management answer such questions as:

- Are there enough current assets to cover current obligations?

- How fast could assets be converted to cash?

- What short-term assets are available for loan collateral?

Another way to evaluate liquidity is the working capital ratio: current assets divided by current liabilities. A healthy working capital ratio varies from industry to industry, but it’s generally considered to be 1.2 to 2. A ratio below 1.0 typically signals impending liquidity problems.

An alternative perspective on working capital is to compare it to total assets and annual revenue. From this angle, working capital becomes a measure of efficiency.

How Is Working Capital Evaluated?

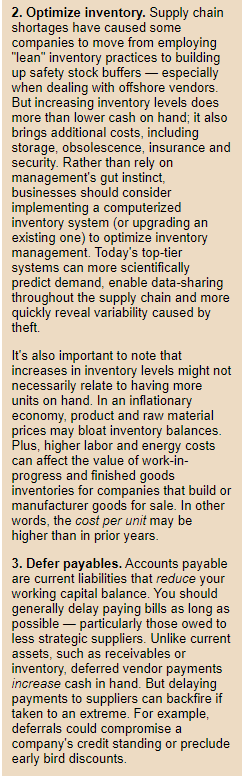

The amount of working capital your company needs — also known as its working capital requirement — is a function of the costs of your sales cycle, upcoming operational expenses and current repayments of debts. Essentially, you need enough working capital to finance the gap between payments from customers and payments to suppliers. To reduce your company’s working capital requirement, you must focus on three key areas: 1) accounts receivable, 2) inventory, and 3) accounts payable. (See “Improving Working Capital Management” at right.)

High liquidity generally equates with low credit risk. But you can have too much of a good thing. Excessive amounts of cash tied up in working capital detract from other spending options, such as expanding to new markets, buying equipment, launching new products and paying down debt. Failure to pursue capital investment opportunities can compromise value over the long run.

How Has the Pandemic Affected Working Capital Levels?

The 2022 Working Capital Survey published by consulting firm The Hackett Group reported improvements in the following working capital metrics over the last two years:

Days sales outstanding (DSO). DSO was down one day in 2021 compared to 2020. That represents a 2% improvement, after deteriorating 2% in both 2019 and 2020. The most significant improvements were reported by business-to-consumer sectors, such as airlines and recreational products.

Days inventory outstanding (DIO). DIO was down one day in 2021 compared to 2020. That represents a 2% improvement, after deteriorating 6% in 2019 and 3% in 2020. However, the survey notes that the results may be skewed by performance in three industries: pharmaceuticals, oil and gas, and biotechnology.

Days payables outstanding (DPO). DPO was up 0.3 days in 2021 compared to 2020. That represents a 2% improvement, after improving by 1.1 days in 2019 and 4.7 days in 2020. The survey concluded that slowed improvement in DPO suggests that companies may have reached the upper limit of payment term extensions during the pandemic.

As a result of these metrics, the average cash conversion cycle (CCC) improved by roughly 6% in 2021 — from 36.5 days in 2020 to 34.2 days in 2021. The CCC equals DSO plus DIO minus DPO. It gauges how efficiently working capital is managed.

Essentially, the CCC accounts for the timing of converting current assets to cash and paying off current liabilities. A positive CCC indicates the number of days a company must borrow or tie up capital while awaiting payment from customers. A negative CCC represents the number of days a company has received cash from customers before it must pay its suppliers.

Working capital management and liquidity did more than just rebound to pre-pandemic levels in 2021. The survey found that the top 1,000 companies have nearly $1.7 trillion tied up in working capital — up 28% from 2020. Although receivables and inventory are down, cash on hand is up. Reportedly, many large companies hoarded cash during the pandemic.

The survey reported that cash as a percentage of revenue rose sharply to 13% in 2020. In 2021, cash on hand fell to roughly 10% of revenue. The survey reports that many companies are spending their cash reserves to clean up operational performance and pay off debt. But this metric also decreased because companies reported higher revenue in 2021 than 2020.

The survey concluded:

While 2021 ushered in a positive reset for working capital performance, conditions are far from normal — and further improvement is far from guaranteed. High inflation and changing consumer demand patterns will likely drive further inventory buildups as companies take preventative actions to protect margins before passing some of the costs to the end consumer. The accelerating workforce availability crisis is creating significant operational problems for manufacturing, hospitality and retail, as well, putting further economic and supply chain recovery at risk. Rising interest rates will increase the cost of capital, keeping cash flow optimization prominently on the corporate agenda in order to provide liquidity for strategic investments. Geopolitical issues and the conflict in Ukraine continue to reverberate in the market. And finally, the pandemic itself is not quite in the rearview mirror. Diligent focus across all three elements of working capital is prudent in this environment.

Government relief measures — including Paycheck Protection Program loans and temporary tax breaks — injected much-needed cash into the markets, helping businesses stay afloat during the pandemic. Now COVID relief has largely dried up, inflation and interest rates are rising, supply chain issues persist, and banks are tightening their underwriting requirements for commercial and industrial loans. These conditions have brought the issue of working capital management to the forefront.

From Analysis to Action

If you feel working capital analysis is out of your league, consider seeking outside expertise. Your financial advisors can help evaluate working capital accounts, identify strengths and weaknesses, and, ultimately, strike a company-specific balance between liquidity safety nets and cash-flow efficiency.