Want to Move? Tax Implications of Converting a Home to a Rental Property

If you’re planning to move out of your current home, you face a tough question: Should you sell your home, or would it be more beneficial to convert it into an income-producing rental property? In terms of both selling prices and rental rates, the residential real estate market has cooled off in many areas. Even so, holding on to your property might seem like a solid investment. There are also tax implications to factor into your decision.

Rental Property Write-Offs

If you decide to convert your home into a rental property, you’ll be able to claim tax write-offs to offset the income. For example, you can deduct mortgage interest and real estate taxes.

You can also write off all the standard operating expenses that go along with owning a rental property. Examples include utilities, insurance, repairs, maintenance, yard care and homeowners’ association fees. In addition, depreciation deductions are a noncash expense that can shelter some or all of your cash flow from federal income tax.

You can depreciate the tax basis of a residential building (not the land) over 27½ years using the straight-line method, while the property may continue to appreciate. Such tax basis may not exceed the fair market value of the property when converted to rental. Your property’s initial tax basis for depreciation purposes usually equals the original purchase price, minus the purchase price allocable to the land, plus the cost of improvements, minus any depreciation write-offs that you’ve claimed over the years. For example, you might have written off depreciation from a deductible home office.

To illustrate the advantages of claiming depreciation, suppose you decide to convert your home into a rental. The tax basis in the property (excluding the land) is $700,000. Your annual depreciation deduction would be $25,455 ($700,000 divided by 27½ years). That means you can have up to $25,455 of positive cash flow each year from your rental property without having to share with Uncle Sam.

Beware of PAL Rules

If your rental property throws off a tax loss, things can get complicated. The passive activity loss (PAL) rules will usually apply. In general, the PAL rules allow you to deduct passive rental losses only to the extent you have passive income from other sources. Examples include passive income from other rental properties or gains from selling them. Passive losses in excess of passive income are suspended until you either have some passive income or you sell the property that produced the losses.

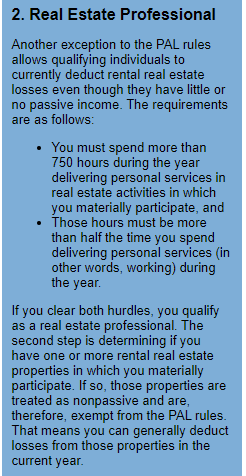

As a result, the PAL rules can postpone rental property loss deductions, sometimes for many years. Fortunately, there are exceptions to the rules that may allow you to deduct losses sooner rather than later. (See “3 Taxpayer Friendly Exceptions to the PAL Rules” at right.)

Taxable Income from Rental Properties

Eventually, your rental property should start generating taxable income instead of losses, because escalating rents may surpass your deductible expenses. Of course, you

In addition, passive income from rental real estate can get hit with the 3.8% net investment income tax (NIIT), along with gains from selling a rental property. The NIIT is on top of the regular income tax rate or regular capital gains tax rate. However, the NIIT only affects people with relatively high incomes. You may owe state income tax, too, if applicable.

must pay income taxes on those profits. But if you piled up suspended passive losses in earlier years, you can use them to offset your current passive profits.

Tax Treatment of Rental Property Sales

The expectation is that you’ll eventually sell a rental property. If so, you’ll have a tax gain to the extent that the net sales price exceeds your tax basis in the property, after adding the cost of any improvements and subtracting depreciation deductions.

If you sell your former principal residence within three years after converting it into a rental, the federal home sale gain exclusion will usually be available. Under that deal, you can shelter up to $250,000 of otherwise-taxable gain (up to $500,000 if you’re married). However, you can’t shelter gain attributable to depreciation deductions. That part of your gain will be taxed at a 25% federal rate.

The tax results without the home sale gain exclusion are still favorable. For example, say you sell a rental property that you’ve owned for more than one year, and the gain exclusion isn’t available. Here, your taxable gain is the difference between the net sales proceeds and the tax basis of the property after subtracting depreciation deductions. The gain qualifies as a long-term capital gain that’s taxed at a federal rate of no more than 20% (23.8% if you owe the NIIT). Again, the amount of gain equal to the cumulative depreciation deductions claimed for the property will be taxed at a 25% federal rate. You may also owe the 3.8% NIIT and state income tax on that part of the gain. You can use any suspended passive losses to offset your gain from selling the property.

Section 1031 Exchange Option

The tax law allows rental real estate owners to effectively sell appreciated property, reinvest the proceeds and defer the federal income hit indefinitely. This strategy is called a Section 1031 like-kind exchange, named for the applicable section of the tax code.

With a Sec. 1031 exchange, you swap the property you want to unload for another property (the replacement property). You’re allowed to defer paying taxes until you sell the replacement property. Or when you’re ready to unload the replacement property, you can arrange another Sec. 1031 exchange and continue deferring taxes.

The Sec. 1031 exchange rules provide flexibility when selecting replacement properties. For example, you can trade holdings in one area for properties in more-promising locations. You could also swap an expensive single-family rental house for a small apartment building, an interest in a strip shopping center or even raw land.

If you die while still owning the replacement property, current law gives your heirs a federal income tax basis step-up to equal the fair market value of the property as of your date of death — or as of six months later if the executor of your estate chooses. So, your heirs can sell the property and owe little or nothing to Uncle Sam.

To Rent or Not to Rent?

Converting a personal residence into a rental property can be a tax-smart move. But it’s not right for every situation, and there’s more to factor into your decision than just taxes. Consult your tax advisor to determine what’s right for you.