What Can You Do to Lower Your 2023 Tax Obligation?

It’s hard to believe that 2023 is already half over. Although summer is a time for vacations and relaxing in the backyard, you can’t afford to take a break from managing your tax bill. Now is a good time to think about proactive moves that could cut your 2023 tax liability. Here are six ideas for individual taxpayers to consider, assuming the current federal tax rules will remain in place through at least 2024.

1. Take Advantage of the Higher Standard Deduction

When filing your federal income tax return, you’ll need to decide whether to itemize or take the standard deduction. The Tax Cuts and Jobs Act (TCJA) significantly increased the standard deduction amounts through 2025 and indexed them annually for inflation. High inflation has had the favorable side effect of increasing the 2023 federal income tax standard deduction allowances that are available if you won’t itemize this year.

For 2023, the basic standard deduction amounts are:

- $13,850 for singles and married couples who file separately,

- $27,700 for married couples who file jointly, and

- $20,800 for heads of households.

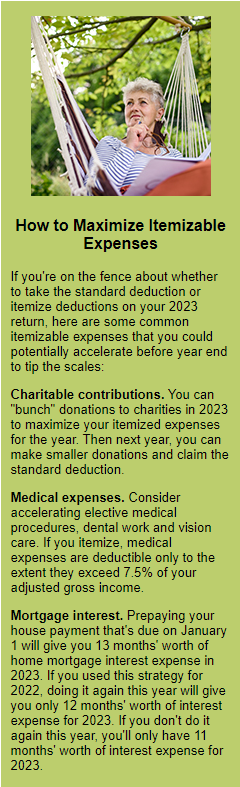

If your total itemizable deductions for 2023 will be close to your standard deduction amount, consider making enough itemized deduction expenditures between now and December 31 to exceed your standard deduction. That will lower this year’s tax bill. Next year, you can always claim the standard deduction, which will be increased again to account for ongoing inflation. (See “How to Maximize Itemizable Expenses,” at right.)

2. Manage Investment Gains and Losses

If you hold investments in taxable brokerage accounts, you may have tax planning opportunities. Consider the following scenarios:

If you have gains. Consider selling appreciated securities that have been held for over 12 months. Long-term capital gains (LTCGs) are taxed at the federal capital gains tax rate, which can be 0%, 15% or 20%. Most individuals will pay 15%. High-income individuals will owe the maximum 20% rate on the lesser of: 1) their net LTCG for the year, or 2) the excess of their taxable income for the year, including any net LTCG,

over the applicable threshold. For 2023, the 20% thresholds are:

- $553,850 for married joint-filing couples,

- $492,300 for single filers, and

- $523,050 for heads of households.

Assuming the current tax rules remain in place for 2024, these brackets will be adjusted for inflation. You also might owe state income tax and the 3.8% net investment income tax (NIIT).

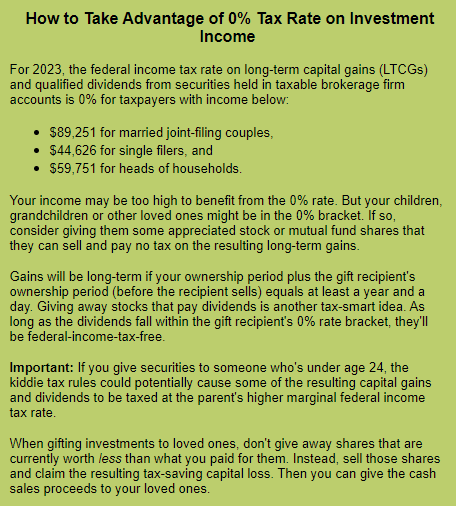

Important: If you’re in the 20% LTCG bracket and you’re feeling generous, you can gift appreciated investments to family members and friends in the 0% bracket. (See “How to Take Advantage of 0% Tax Rate on Investment Income,” below.)

If you have losses. To the extent you have capital losses that were recognized earlier this year or capital loss carryovers from previous years, selling appreciated shares this year won’t result in any tax hit. In particular, sheltering net short-term capital gains with capital losses is a tax-smart move, because net short-terms gains would otherwise be taxed at higher ordinary-income rates.

If you have some losing investments that you’d like to sell, consider taking the resulting capital losses this year to shelter capital gains, including high-taxed short-term gains, from other sales in 2023.

If selling a bunch of underperforming investments would cause your capital losses to exceed your capital gains, the result would be a net capital loss for the year. In this situation, your net capital loss could shelter up to $3,000 of 2023 ordinary income from tax ($1,500 if you use married filing separately status). Ordinary income includes salaries, bonuses, self-employment income, interest and royalties.

Any excess net capital loss from this year is carried forward indefinitely. The carryover can be used to shelter both short-term and long-term gains recognized next year and beyond. This can give you extra investing flexibility in those years because you won’t have to hold appreciated securities for over a year to get a lower tax rate. Moreover, the top two federal rates on net short-term capital gains recognized in 2024 are expected to remain at 35% and 37% (plus the 3.8% NIIT, if applicable). So having a capital loss carry over into next year to shelter short-term gains recognized next year could be advantageous.

3. Donate to Charity

If you itemize and want to make gifts to your favorite charities before year end, you can make them while also adjusting your taxable account investment portfolio. Consider making charitable contributions with these tax-smart principles:

If you have long-term gains. Donate appreciated investments instead of giving away cash. For itemizers, donations of publicly traded shares owned over a year result in charitable deductions equal to the full current market value of the shares at the time of the gift. Plus, if you donate shares that are worth more than you paid for them, you escape capital gains taxes that would result from a sale.

If you have losses. Sell investments that are worth less than you paid for them and collect the resulting tax-saving capital losses. Then give the cash sales proceeds to favored charities and, if you itemize, claim the resulting tax-saving charitable contribution deductions.

4. Convert a Traditional IRA into a Roth Account

If you expect to be in the same or higher federal income tax brackets during retirement, a Roth IRA conversion could be a tax-smart move. The current tax hit from a conversion done this year could be a relatively small price to pay for avoiding potentially higher future federal tax rates on the account’s earnings. In effect, a Roth IRA can insure part or all of your retirement savings against future federal tax rate increases.

A Roth conversion is treated as a deemed distribution of your traditional IRA balance with a subsequent deemed contribution to the Roth account. So, it will generally trigger a current federal income tax bill and possibly state income tax. You’ll need to have enough cash on hand to pay the taxes.

5. Defer Income into Next Year

You might be able to defer some taxable income from this year into next year, thereby delaying the related income tax. Because the thresholds for next year’s federal income tax brackets will likely increase thanks to inflation adjustments, the deferred income might be taxed at a lower rate than would apply for 2023.

This strategy works only in limited situations. For example, a sole proprietor might delay billing customers until after January 1, 2024, for work completed near year end. Or an employee might ask his or her employer to delay paying bonuses until after January 1, 2024.

6. Cash In on Principal Residence Gain Exclusion Break

Home prices in some areas have cooled off. But you still might be sitting on a significant unrealized gain. If so, what’s the tax treatment if you sell to downsize, upsize or move to another area?

An unmarried person may be able to exclude up to $250,000 of gain on the sale of his or her principal residence from federal income tax. But the home sale gain exclusion can be worth twice as much for a married couple if certain conditions are met. (The limit for qualifying married individuals who file separate returns is only $250,000, however.)

To qualify for the gain exclusion break, you generally must have owned and used the home as your principal residence for at least two years during the five-year period ending on the sale date. Your tax advisor can explain how to take full advantage of this tax break, as well as the state income tax considerations, if applicable.

What’s Right for Your Situation?

These ideas are just the tip of the tax-saving iceberg. There are other opportunities for individuals, including education-related breaks, tax-favored treatment for health savings accounts, and credits for energy-efficient home improvements and vehicles. Contact your tax advisor for more information on these and other midyear tax-saving strategies.